Uptick Insight Series | 6 Ways RWA 2.0 Is Different From Everything

That Came Before

Published on Mar 17, 2026

When Blockchain Capital published its first serious analysis of RWA

tokenization in 2019, the framing was almost entirely about

representation, about taking a bond or a property deed and creating a

digital token that proved ownership on-chain, settling faster, moving

more freely, and essentially, costing less to administer than the

paper-based systems it replaced.

That framing captured something real but actually missed something

larger, because the conversation was almost entirely surrounding what

the token represented rather than what it could do, treating

tokenization as a more sophisticated cabinet for ownership records

rather than as programmable infrastructure capable of reshaping how

assets generate value, reach investors, and respond to the communities

that own them.

It’s been a long ride…

The market spent six years and billions of dollars in that first

phase, and the results were instructive. A 2025 arXiv study examining

more than $25 billion in on-chain tokenized assets found that most of

them exhibited low trading volumes, long holding periods, and minimal

secondary market activity, which is the financial equivalent of

building a motorway that nobody bothers to drive on.

The RWA market is now moving through a completely different phase, one

the industry is starting to call RWA 2.0, shifting from conceptual

exploration to the harder work of building infrastructure that

actually functions. With this shift, it’s exposing a clear dividing

line between platforms that tokenized assets and platforms that built

the complete infrastructure stack needed to make those assets function

as genuine financial instruments in the real economy.

The problem was never the tokenization layer, it was that every other

layer of infrastructure needed to make a tokenized asset business

actually work, the rights confirmation, the on-chain valuation, the

profit sharing, the trading infrastructure, the risk disclosure, was

either missing entirely or rebuilt from scratch by each issuer at

enormous cost and inconsistent quality, creating a market full of

tokens that technically existed but practically underdelivered on

almost every dimension that mattered to the businesses and investors

they were supposed to help.

RWA 2.0 is the recognition that a token without the complete

surrounding infrastructure is not a financial product, it is simply a

proof of concept, and that building the standardized, scalable

infrastructure stack connecting the real economy to on-chain finance

is the actual work this market has been building toward since the

first bond settled on-chain back in 2020.

In this article, we’re going to explore six ways that distinction is

changing everything.

Let’s get into it.

The defining limitation of first-gen tokenized assets was that they

were structurally isolated, meaning that the token existed on-chain

but the entire system around it (valuation, income distribution,

performance reporting, risk disclosure, etc), stayed off-chain,

managed by the same fund administrators and intermediaries who managed

it before tokenization existed, operating on their schedules and

according to their incentives.

Income distribution required manual calculation, and valuation updates

arrived quarterly in PDF reports prepared by third parties whose

incentives weren’t necessarily aligned with accuracy over

presentation. Risk disclosure was whatever the issuer chose to include

in a document that investors received once rather than a live data

feed they could query at any time, and the token itself had zero

awareness of how the underlying asset was actually performing at any

given moment.

BlackRock’s BUIDL fund and MakerDAO’s RWA collateral positions are the

two most cited examples of Web3 financial products in the current

market, and both confirm the same pattern. Despite their on-chain

presence, both maintain relatively static liquidity profiles, are held

for yield rather than actively traded, and continue to depend on

off-chain systems for the operational logic that actually governs

investor experience.

This tells us that the tokenization layer works, but everything around

it still runs the old way.

RWA 2.0 treats the token not as the product but as the entry point

into a complete on-chain system covering rights confirmation,

continuous valuation, automated profit sharing, active trading

infrastructure, and transparent risk disclosure, all of which need to

work together as an integrated stack rather than as separate pieces

assembled differently by every issuer who comes to market.

The practical significance of standardization here is easy to

underestimate. When every RWA issuance requires a custom technical

build to connect the asset’s economic logic to its on-chain

representation, the market stays limited to well-capitalized

institutional issuers who can afford that build, and the vast majority

of real-world assets that could benefit from tokenization never make

it to market because the barrier is too high. Standardized contract

templates and data specifications that lower the threshold for

physical assets to enter Web3 are what transform tokenization from an

institutional experiment into a scalable market.

Uptick’s Programmable NFT Protocol and DeFi Protocol provide the

foundation for this core financial logic, because programmable NFTs

are able to carry dynamic metadata that updates continuously as asset

conditions change, smart contracts embedded in the token execute

income distribution automatically when predefined conditions are met,

and the ability to connect to a DeFi Protocol’s NFT collateralization

and leasing standards let these same assets participate in broader

financial markets rather than sitting idle between income events.

The asset stops simply representing ownership, and actively manages

the economic relationship between the underlying business and every

investor who holds a stake, with the full valuation, profit-sharing,

and risk disclosure stack operating on-chain rather than through

intermediaries who charge for doing it slowly and selectively.

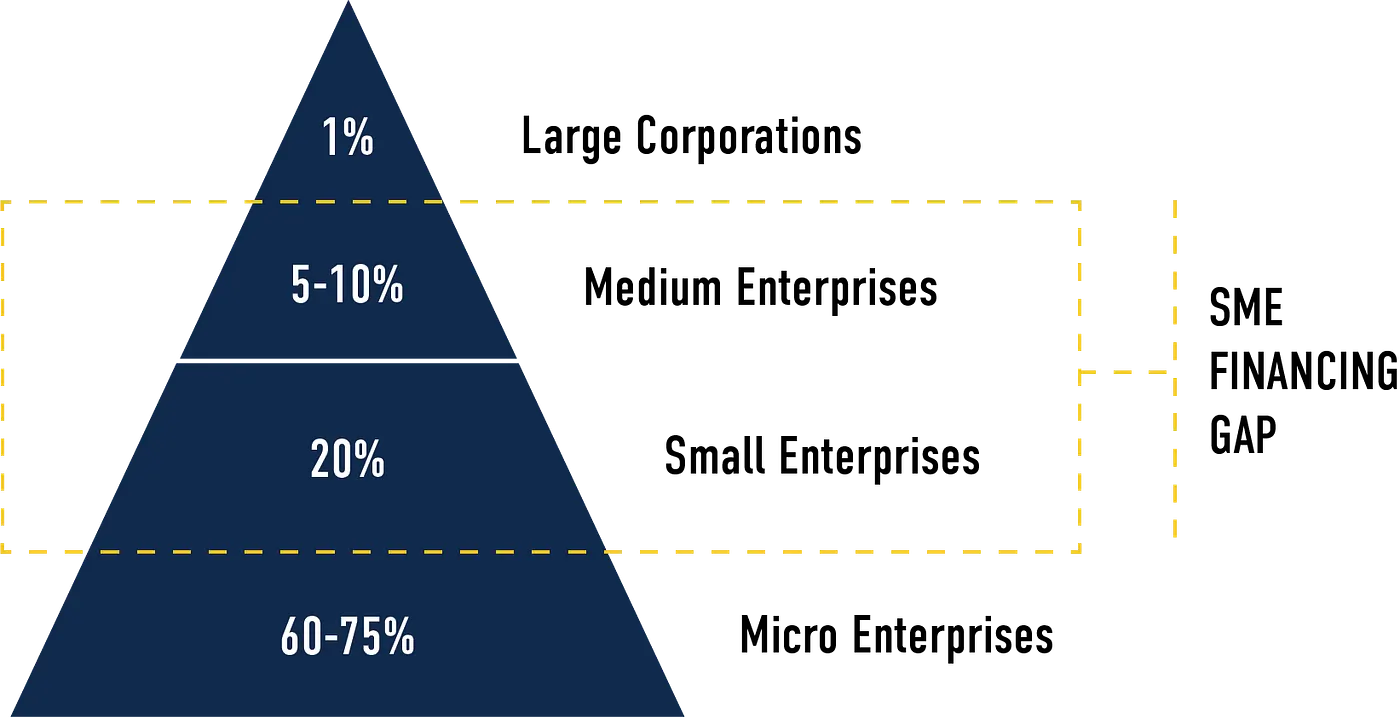

Small and medium-sized businesses collectively represent the backbone

of most economies, but access to working capital financing for SMEs

remains one of the most persistent failures in global finance, with

the Asian Development Bank estimating a $2.5 trillion annual trade

finance gap affecting primarily smaller businesses whose assets are

real but whose data is too broken and difficult to verify for

traditional lenders to comfortably extend credit.

The problem isn’t that these businesses lack genuine assets, a

manufacturer with confirmed purchase orders from creditworthy buyers

has a real claim on future cash flows, a trading company with

warehouse receipts for physical inventory holds an asset with

verifiable value, and an agricultural producer with forward contracts

for the coming harvest has documented revenue that any rational lender

should advance against.

Platforms like Maple Finance, Centrifuge, and Goldfinch have show us

that appetite for tokenized SME credit is genuine, with active

on-chain private credit exceeding $18 billion by late 2025, but the

businesses accessing that capital have mostly been those with

sophisticated enough legal and technical teams to navigate the custom

build required to get their assets on-chain in the first place. The

SME in Southeast Asia with real warehouse receipts and no blockchain

development budget is still locked out, not because global investors

wouldn't fund them, but because nobody built the infrastructure to

make the connection simple enough to use.

Tokenization changes the verification equation entirely when it's

built on the right infrastructure. When an SME’s trade assets are

tokenized on-chain with their authenticity, performance status, and

fund flows made continuously verifiable through Uptick’s planned

Oracle feeds, the verification burden that previously required

expensive manual due diligence gets replaced by transparent data that

any investor can query directly, and the geographic barriers that

limited financing to whoever was physically close enough to verify the

assets collapse because on-chain verification works the same whether

the investor is local or on the other side of the world.

Uptick’s infrastructure supports deployment across public blockchains

and compliant ecosystems via its modular architecture, with the Uptick

Cross-chain Bridge (UCB) handling interoperability between them, which

means an SME asset could, in theory, eventually meet the compliance

requirements of its home jurisdiction and still remain accessible to

global investors operating across different blockchain ecosystems,

rather than forcing issuers to choose between regulatory compliance

and investor reach.

Uptick's Decentralized Data Service addresses the verification layer

by storing asset performance data with cryptographic permissioning, so

the manufacturer's purchase order status, the trading company's

warehouse receipts, and the agricultural producer's forward contracts

are all continuously verifiable by any investor who needs to assess

them, without exposing sensitive business information to parties who

don't have a legitimate need for it.

Combined with the Omnichannel Payment Module supporting multiple

currencies and stablecoins, an SME in Southeast Asia might access

financing from a capital pool spanning multiple ecosystems

simultaneously, receiving working capital at competitive rates from a

global investor base that previously had no practical way to reach

them.

This is what it means for RWA to serve the real economy rather than

financial speculation, because the capital flows to businesses that

need it to operate and grow rather than to instruments that exist

primarily to give sophisticated investors another vehicle for yield

optimization.

Every serious discussion of RWA market growth eventually arrives at

the same bottleneck, which is that secondary market trading in

tokenized assets is suppressed not by lack of investor interest but by

compliance friction that makes transferring tokens between investors

more operationally complex than it should be.

The arXiv study confirmed this directly, noting that participation in

most tokenized RWAs is restricted to whitelisted KYC-compliant

addresses, and that this whitelisting requirement is one of the

primary structural barriers keeping secondary markets thin regardless

of how much underlying investor demand exists.

The traditional approach treats compliance as a gateway, a wall that

investors pass through during onboarding and again whenever a transfer

involves a new counterparty, with human compliance teams reviewing

documentation and administrators maintaining whitelists that determine

which wallets are permitted to hold which assets. This works tolerably

for primary issuance where the investor set is small and transactions

are infrequent, and it breaks down almost completely for secondary

markets where the value proposition depends on investors being able to

transact freely as conditions change.

The architectural fix is embedding compliance into the token itself

rather than layering it on top as a separate manual process, so that

transfer rules, investor eligibility requirements, and jurisdictional

restrictions become part of the asset’s smart contract logic that

executes automatically rather than triggers a human workflow that

takes days and costs money every time it runs.

Uptick DID makes this practical by allowing investors to carry

verifiable credentials built on W3C standards that prove their

compliance status and jurisdictional eligibility through selective

disclosure, meaning an investor can demonstrate everything a transfer

requires without exposing their full identity to every counterparty.

When those credentials are cryptographically linked to the

Programmable NFT Protocol’s access control mechanisms, transfers

complete automatically when both parties carry valid credentials and

are blocked automatically when they don’t, creating a compliance layer

that runs at the speed of code.

Secondary market activity then stops being a compliance problem and

starts being a business advantage.

The single most underappreciated structural problem in the current RWA

market is chain fragmentation, where an asset tokenized on Ethereum

can only be owned by Ethereum investors, leaving out every dollar

sitting in Cosmos-based DeFi protocols, Binance Smart Chain

ecosystems, and Polygon liquidity pools that might otherwise find the

asset attractive.

The consequences are measurable, as research tracking tokenized RWA

markets in 2025 documented 1 to 3% pricing gaps for identical assets

held across different chains, and 2 to 5% friction costs when moving

capital cross-chain, meaning that chain fragmentation isn’t just an

inconvenience, it is actively destroying value for both issuers and

investors who have no mechanism to close the gap without expensive

manual bridging that often introduces new compliance complications on

the other side.

For an issuer, this means the size of your investor base is determined

not by who finds your asset attractive but by which chain you happened

to build on, and there is no market logic that justifies that

constraint.

A real estate fund issuing tokens on Ethereum in 2021 and a private

credit vehicle issuing on a Cosmos chain in 2023 are both tokenized

assets serving investors who might rationally want exposure to both,

but those investors are currently forced to manage separate wallets,

separate on-ramps, and separate compliance processes for each

ecosystem, which is friction that suppresses participation and keeps

secondary markets thinner than the underlying investor demand would

support if the infrastructure got out of the way.

Uptick’s Cross-chain Bridge (UCB) and IBC protocols resolve this at

the infrastructure level, enabling tokenized assets to move freely

across Ethereum, Cosmos, Binance Smart Chain, and Polygon ecosystems

(and more), through the same underlying architecture rather than

requiring each issuer to negotiate their own bridging arrangements

with every ecosystem they want to reach.

For an RWA business, the secondary market for their asset becomes as

large as the combined investor base across all those ecosystems rather

than one slice of one chain, and the UCB’s use of zk-SNARK

verification for off-chain computation means cross-chain transfers

stay cost-efficient even at the transaction volumes that genuine

secondary market liquidity requires.

One of the most consistent failures in first-generation RWA platforms

was treating token issuance as the conclusion of the business process

rather than the beginning of an ongoing relationship, leaving issuers

with essentially no tools for engaging token holders after capital was

raised, no mechanism for rewarding long-term commitment, and no

structured way to build the kind of community around an asset that

turns investors into advocates who bring in additional capital over

time.

An analysis of common RWA business failures identified the top three

operational mistakes as launching without a clear liquidity plan,

ignoring KYC and AML obligations, and underestimating the need for

investor communication during downturns, and noted that each of these

kills momentum faster than any technical failure. The third one is

pretty telling, because it’s not a technical problem, it’s a

relationship problem, and the platforms that experienced it the

hardest were the ones that had no infrastructure for maintaining

investor relationships beyond the quarterly report and the occasional

email when something went wrong.

A token holder who bought into a real estate fund during a

distribution drought has no visibility into what management is doing

about it, no channel to ask, and no reason to hold rather than exit at

a loss, and the platform has no way to know any of that is happening

until the redemption request arrives.

Uptick’s Decentralized CRM stores investor interaction data across its

decentralized infrastructure, using IPFS for off-chain storage with

cryptographic access controls and on-chain records to keep

immutability and transparency, giving RWA businesses the ability to

see when engagement is dropping and respond through automated smart

contract logic before a disengaged holder becomes a redemption

request, rather than discovering the problem only after it has already

happened.

A fund might want to automatically unlock enhanced reporting access

for investors who have held tokens through multiple distribution

cycles, issue governance weight proportional to holding duration, or

distribute bonus yield allocations to token holders who participate

actively in governance votes, all running automatically through

programmable logic without operational overhead.

The Decentralized CRM extends this further by enabling RWA businesses

to create tiered investor experiences where different holding levels

unlock genuinely different access, issuing loyalty rewards as NFTs

when defined conditions are met, granting enhanced governance

participation to long-term holders, and giving the most committed

investors secondary market privileges through programmable smart

contract logic.

These are programmable economic relationships that give investors

concrete reasons to deepen their commitment rather than treating every

investor identically regardless of how much value their long-term

participation creates for the platform.

The governance problem in tokenized assets is a direct inheritance

from traditional fund structures where decision-making authority sits

entirely with the general partner or asset manager, and investors who

disagree with a decision have essentially two options, accept it or

redeem, with no structured mechanism for collective input, no

transparent record of how decisions were actually made, and no binding

process for resolving disputes that doesn’t involve lawyers and years

of litigation.

Legal analysis of tokenized fund governance published in 2025

identified a specific and recurring problem, which was that unless

smart contract voting logic is audited and legally referenced in the

offering documents, it stays legally unclear which version of the code

governs investor rights in a dispute, meaning most tokenized assets

currently carry governance infrastructure that is either absent

entirely or legally unenforceable when it actually matters.

There was also the Brickken survey that confirmed the business

consequence, with governance and investor rights ranking among the top

concerns cited by institutional investors evaluating tokenized asset

platforms in late 2025.

Uptick’s Social DAO infrastructure gives RWA businesses the ability to

encode genuine governance rights directly into their token structures,

where holders propose and vote on material decisions through smart

contracts that execute outcomes automatically when votes reach defined

thresholds and record every decision immutably on-chain.

This makes the governance history of an asset permanently transparent

and auditable by any investor or regulator who needs to understand how

it has been managed.

Combined with Uptick DID, governance participation stays compliant

without becoming a burden, and verified investor identities are

cryptographically linked to governance tokens so only eligible holders

participate in each vote, jurisdictional restrictions are enforced

automatically, and individual voter privacy is protected through

selective disclosure that confirms eligibility without exposing

personal data to other participants.

The business case goes beyond compliance and investor satisfaction,

because a community of token holders who genuinely shape the direction

of an asset become fundamentally different participants than passive

investors waiting for distributions, and that difference shows up in

referral rates, reinvestment decisions, and the kind of organic

community growth that no marketing budget can replicate because it

comes from investors who feel genuine ownership over something they

helped build.

The $24 billion RWA market of 2025 was built largely on

first-generation infrastructure, which was good enough to prove the

concept but not good enough to deliver on its full potential,

As the gap between tokenization as a filing system and tokenization as

a complete programmable economic infrastructure remained wide enough

that most tokenized assets never developed the secondary market depth,

investor engagement, and the strength of the operation that justified

the complexity of putting them on-chain in the first place.

RWA 2.0 closes that gap by treating the token as the entry point into

a complete infrastructure stack rather than the product itself,

building the rights confirmation, the on-chain valuation, the profit

sharing, the compliance layer, the cross-chain liquidity, the investor

relationship management, and the governance tooling into the

foundation rather than leaving each issuer to reconstruct it

independently at a cost that keeps the real economy locked out of a

market that was supposed to serve it.

Whether it’s the SME with genuine trade assets and no access to global

capital, the real estate fund that wants investors across multiple

ecosystems rather than one, or the investor who wants genuine

governance rights rather than quarterly PDFs all require the same

thing, we are creating infrastructure that is standardized and

scalable enough to connect the real economy to on-chain finance

without demanding that every participant rebuild it from scratch.

That infrastructure is what RWA 2.0 actually is, and building it is

what Uptick has been working towards from the beginning.