Web3 Infra Series | The Confidence Layer Missing From Tokenized Asset

Markets

Published on May 27, 2026

One of the strangest things about the RWA market is how often people

conflate transferability with liquidity. They're not the same thing,

and the gap between them is where most of this space is currently

stuck.

You can tokenize an asset, put it on-chain, make it technically

movable between wallets, list it somewhere that has the visual grammar

of a market, and still end up with nothing that resembles actual

trading. Secondary demand doesn't follow from transferability, and it

never has.

The assumption underlying most RWA launches is that once the token

exists, the liquidity problem becomes a distribution problem. Get

enough people to see it and trading follows, but that framing is wrong

in a specific way. It treats the first buyer's due diligence as a sunk

cost rather than a recurring one, so every new buyer has to rebuild

confidence in the asset more or less from scratch, and if the

information needed to do that is spread out, expensive to verify, or

just absent, most of them won't bother.

This results in the token just sitting there, and the market staying

thin, and that's not a token design problem, it's a legibility

problem, which compounds the longer it goes unaddressed.

What Uptick is building, even when it isn't framed this way

explicitly, is that on-chain records, readable payment history, and

traceable governance do something specific for secondary market

formation. They make the asset cheaper to understand for each

successive buyer, which is different from making it easier to

transfer, and that's what actually matters for liquidity, because it

lowers the cost of the confidence-building every buyer has to do

before they step in.

In this article we're going to explore why legibility is the missing

layer in most RWA deployments, and how Uptick's infrastructure

approach is aiming to solve it.

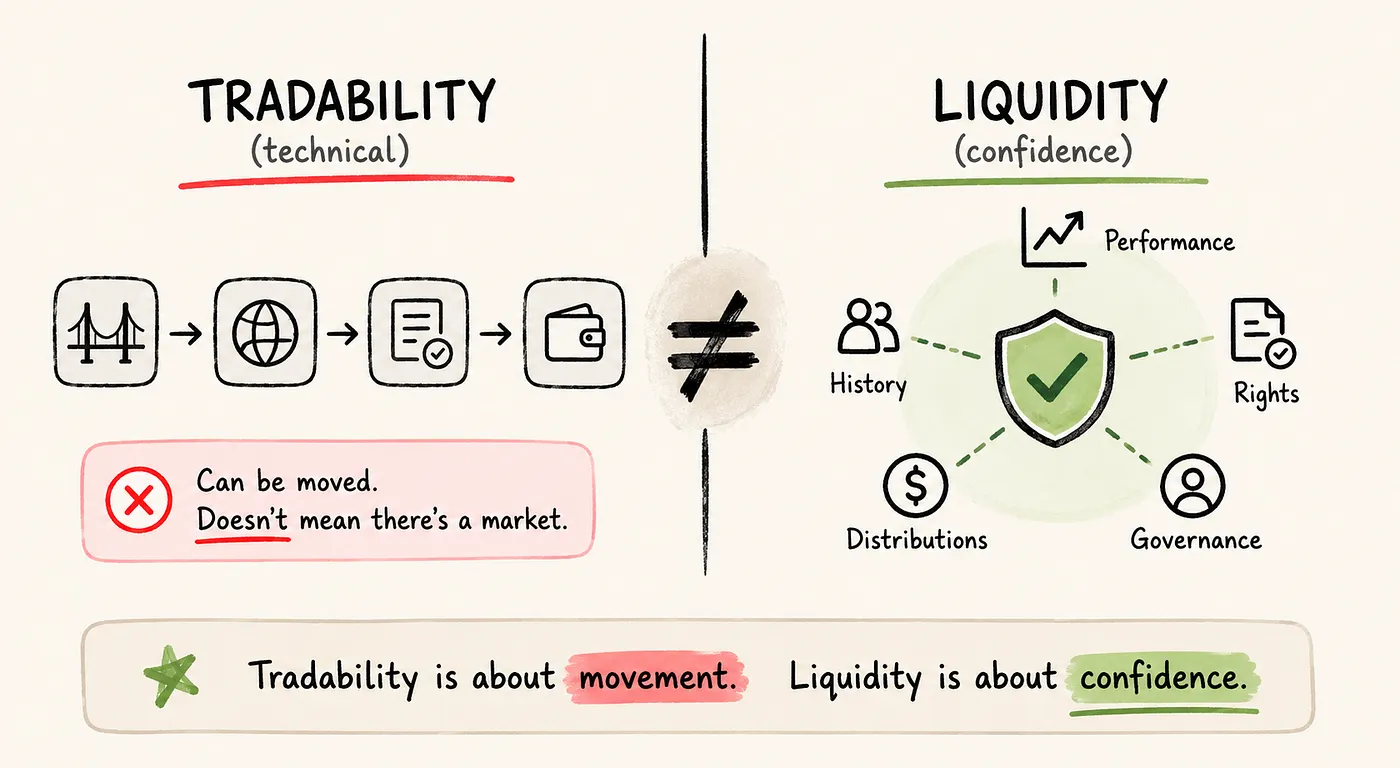

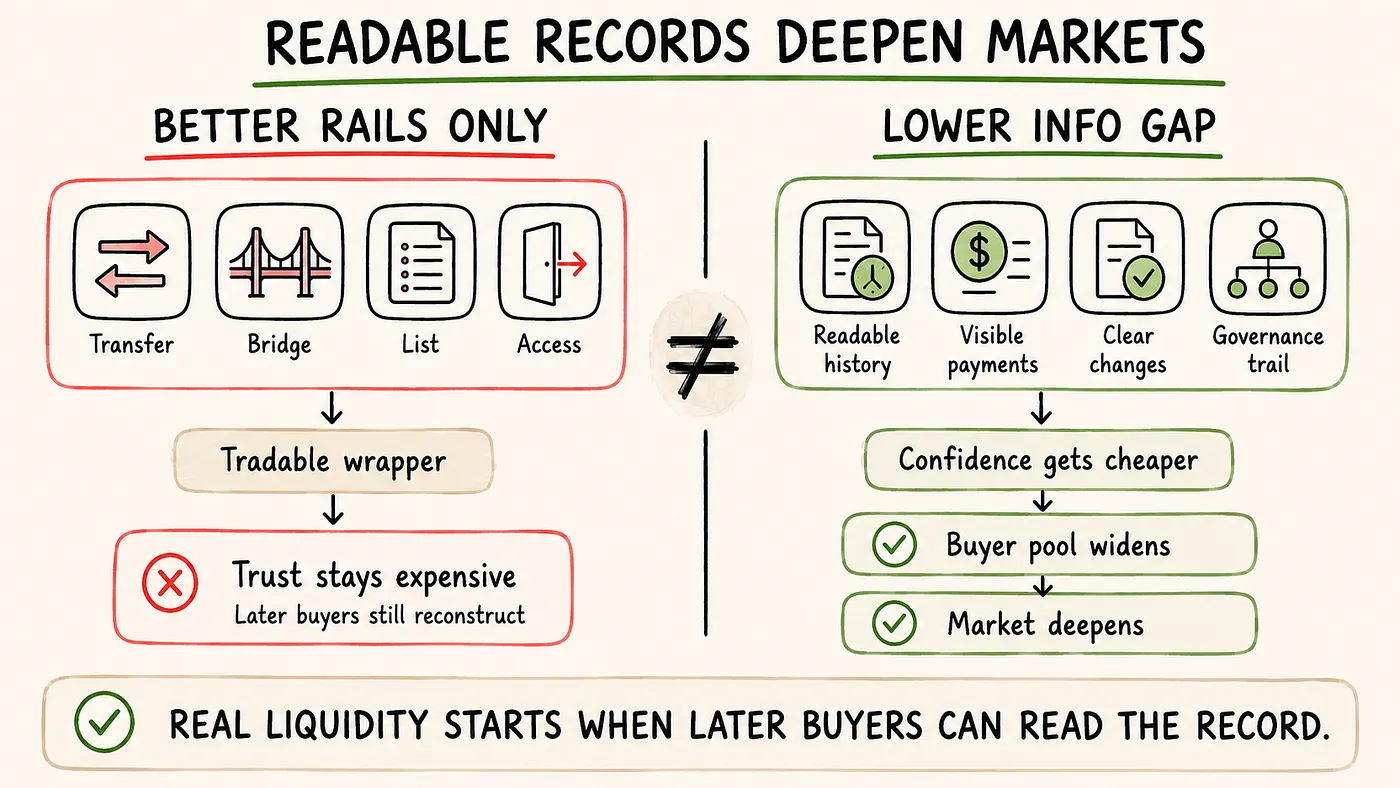

The market still gives too much credit to movement.

If a token can be transferred, bridged, listed, or made technically

available across systems, that gets treated as progress toward

liquidity, but it's really just progress toward tradability, and those

are not the same thing.

Tradability is a technical condition and liquidity is a confidence

condition, and most of the infrastructure being built right now is

solving for the first one and assuming the second will follow.

A buyer looking at a tokenized asset in a secondary market isn't

simply asking whether the token can be received and held, they want to

know how the asset has behaved, how value has moved through it, how

decisions have been made, whether rights are clear, whether

distributions have been reliable, and whether the whole thing still

makes sense without leaning too heavily on whoever is selling it.

That is a completely different burden from transferability, and it's

the one that actually determines whether a market feels real.

This is why so many tokenized assets still don't feel truly liquid,

because the transfer layer has improved considerably, but the

confidence layer is still too weak, and if every new buyer has to

rebuild the whole case from scratch, the market stays narrow. There

could be a few informed holders and occasional trades between a

handful of participants, but that's not a secondary market with any

real depth.

Most business owners understand this instinctively, which is why a

product isn't easier to sell just because it can be shipped, and a

business isn't easier to finance just because the legal paperwork

exists, because in both cases the buyer still has to feel confident

enough to move.

Tokenized assets work the same way, and the ability to transfer is

necessary but nowhere near sufficient.

This is one of the clearest reasons liquidity stays thinner than

people expect.

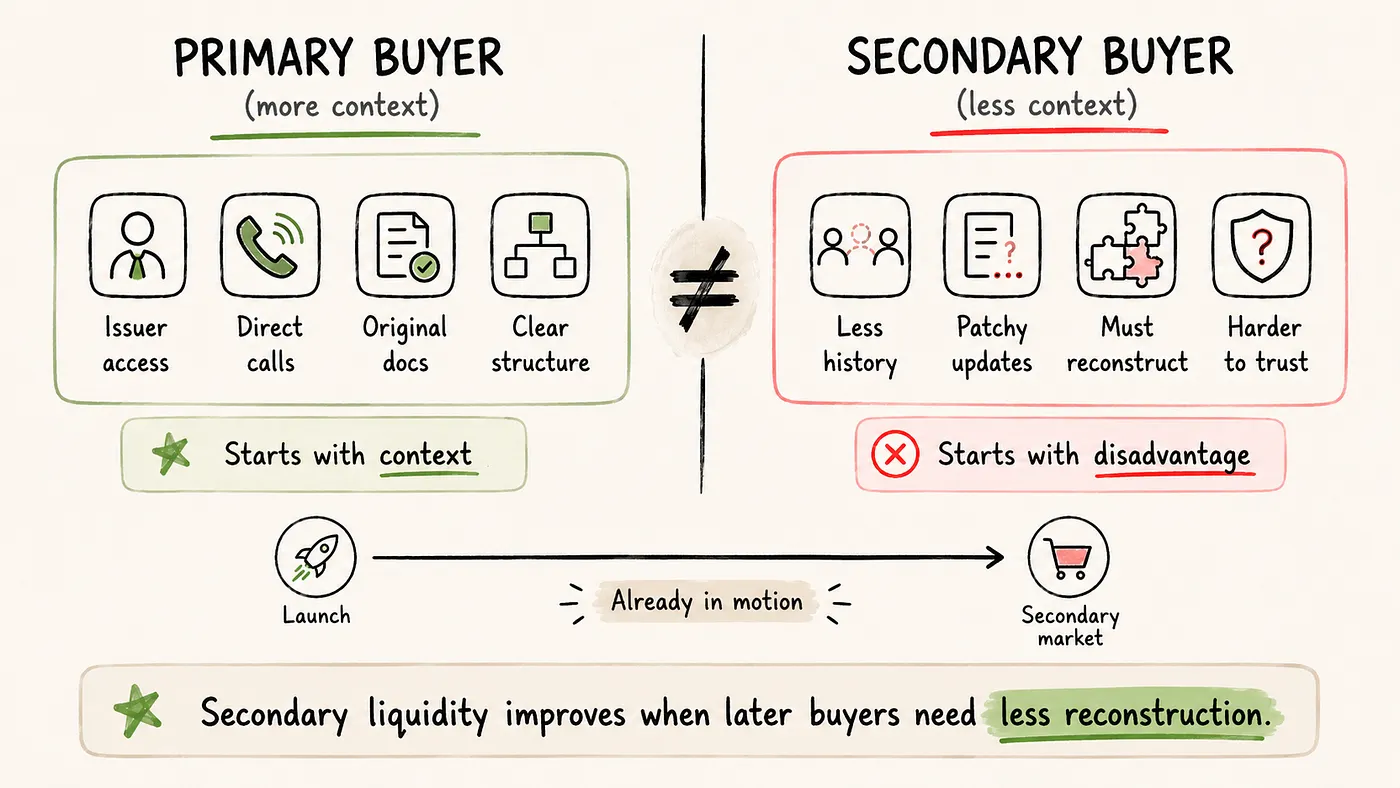

The first buyer often knows the issuer better, may have been closer to

the initial raise, and likely had direct conversations, custom

documents, and a cleaner understanding of how the asset was structured

from the start, but the second buyer usually gets much less than that,

and it changes the economics of trust immediately.

A secondary buyer is stepping into something already in motion, so

they need to understand not just what the asset is but what has

happened since launch, whether distributions kept arriving, whether

governance has been stable, whether the asset has behaved as expected,

and whether there have been material changes or signs that the whole

thing has become harder to read over time.

If that record is weak, secondary demand weakens with it.

This is one reason the old idea about tokenization creating liquidity

has always felt too loose. Tokenization creates the possibility of a

transfer, and secondary liquidity only starts becoming real when later

buyers can enter with less informational disadvantage than they would

have had in a traditional structure. If they still need to do

significant reconstruction, the asset stays technically tradable but

feels commercially heavy.

That's exactly where Uptick's RWA 2.0 infrastructure makes a more

concrete argument than most of what's circulating in this space.

First-generation tokenized assets ignored provenance and track record,

which produced tokens that functioned technically but failed to

attract secondary market depth because investors couldn't verify

performance independently.

Uptick's approach treats on-chain history as a core component of asset

value rather than a byproduct of it, handling continuous

tamper-resistant performance records, portable compliance credentials

that reduce the need to keep rebuilding verification context,

automated on-chain distribution records, and transparent governance

trails. Each passing cycle adds to that record, and that accumulation

is what makes the asset cheaper to evaluate for each successive buyer,

because more of the information needed to build confidence is already

attached to the asset, rather than needing to be reconstructed from

square one.

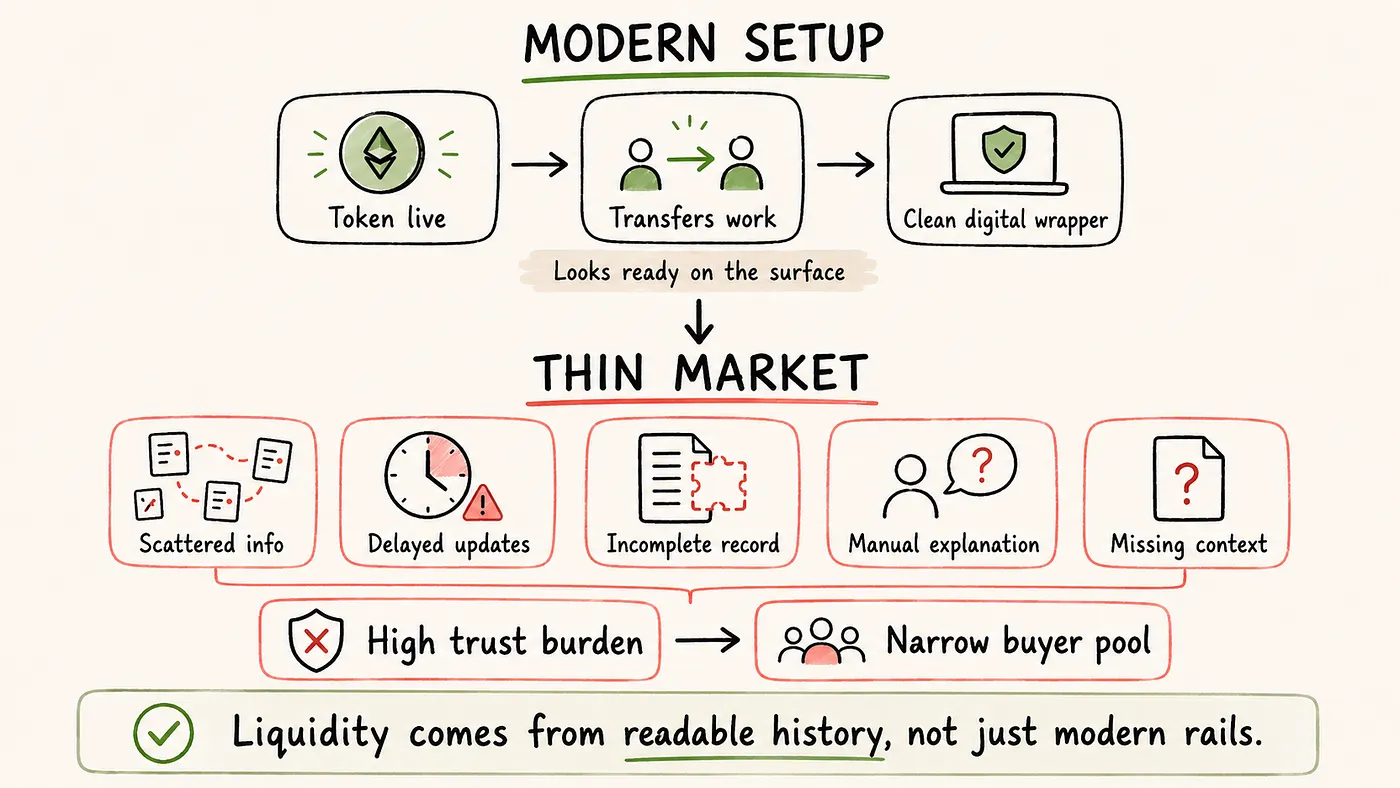

The market starts feeling thin here even when the infrastructure looks

modern.

A later buyer shouldn't need to trust the issuer's presentation more

than the asset's own record, and that's the point most tokenized

assets still haven't reached. The token may be live, the transfer

logic may work, the asset may sit in a digital form that looks clean

enough on the surface, but if the surrounding information is

disconnected, delayed, incomplete, or too dependent on manual

explanation, the buyer is still being asked to extend a level of trust

that most won't.

It shows up in familiar ways. Trust that distributions happened as

described, that the operational record is complete, that performance

updates reflect the full picture, that governance was sound, that no

important context is missing, that the asset remains structurally

healthy even if the reporting doesn't make that obvious. Each one of

those is a gap the buyer has to bridge on their own, and when enough

of them stack up, later buyers start stepping back, not always because

the asset is weak, but because the informational burden is too high

relative to the benefit of entering.

If the market asks a buyer to do too much interpretation, the asset

starts feeling less like a market instrument and more like a private

arrangement with a token attached to it. A liquid market doesn't

eliminate trust, it reduces the amount of blind trust required, and it

does that through visibility, continuity, and enough readable

operating history that later participants can enter without being

forced into a highly asymmetric position.

Once the cost of confidence stays high, the market stays narrow

regardless of how often people say the word liquidity.

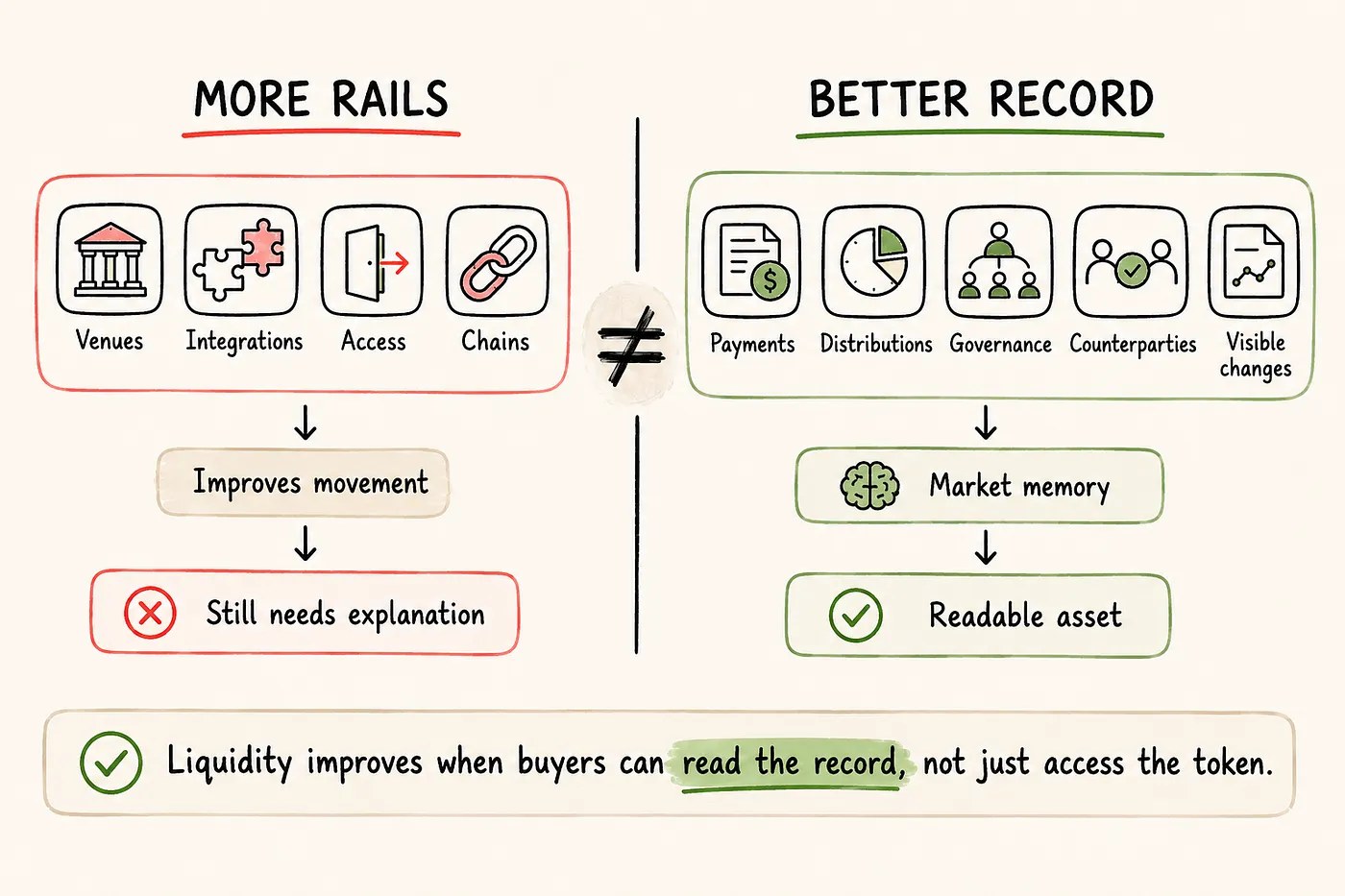

The easy mistake is to think the market mainly needs more venues, more

integrations, more access points, or more chains.

Sometimes it does, but quite often it needs something less exciting,

like a better record. A later buyer wants to know what the asset has

done, not just that it exists. Whether payments flowed consistently,

distributions arrived on time, counterparties remained stable,

governance decisions were visible, and the asset was managed in a way

that builds confidence rather than eroding it. If something went

wrong, was it visible. If expectations changed, was that recorded

clearly. If the asset has moved across systems, did the history travel

with it in a form that still makes sense. That's what gives a

secondary market something to stand on.

Without that layer, buyers remain too dependent on packaging, and

they're not reading an asset, they're reading somebody's current

explanation of the asset, which is much weaker ground.

This is where the stronger RWA infrastructure picture becomes more

interesting than the basic concept of tokenization. A token by itself

doesn't create a market memory, and market memory comes from an

operating trail that is visible enough, durable enough, and coherent

enough to reduce the amount of re-explanation needed each time a new

buyer appears.

Uptick's broader stack starts making a lot more sense for the same

reason.

When you have decentralized data services, omnichannel payments,

governance records, DID-linked access logic, and cross-chain movement,

they are only important if they help preserve the readability of the

asset as it moves through time and across environments. If that

readability stays weak, the transfer layer may improve but the market

still feels thin, and if it improves, the asset starts feeling less

issuer-dependent and more market-readable, which is a much stronger

basis for liquidity than saying the asset is now tradable.

A lot of secondary market confidence gets built through payments.

The market still tends to treat this as an administrative layer rather

than as evidence, which is where a lot of value gets left behind. For

a buyer entering later, payment history is one of the clearest signals

available. Whether investors received what they were supposed to

receive, whether distributions arrived cleanly, whether fund flows

behaved as described, whether the asset kept doing what the structure

said it would do. Those questions matter because they collapse a lot

of ambiguity into something concrete.

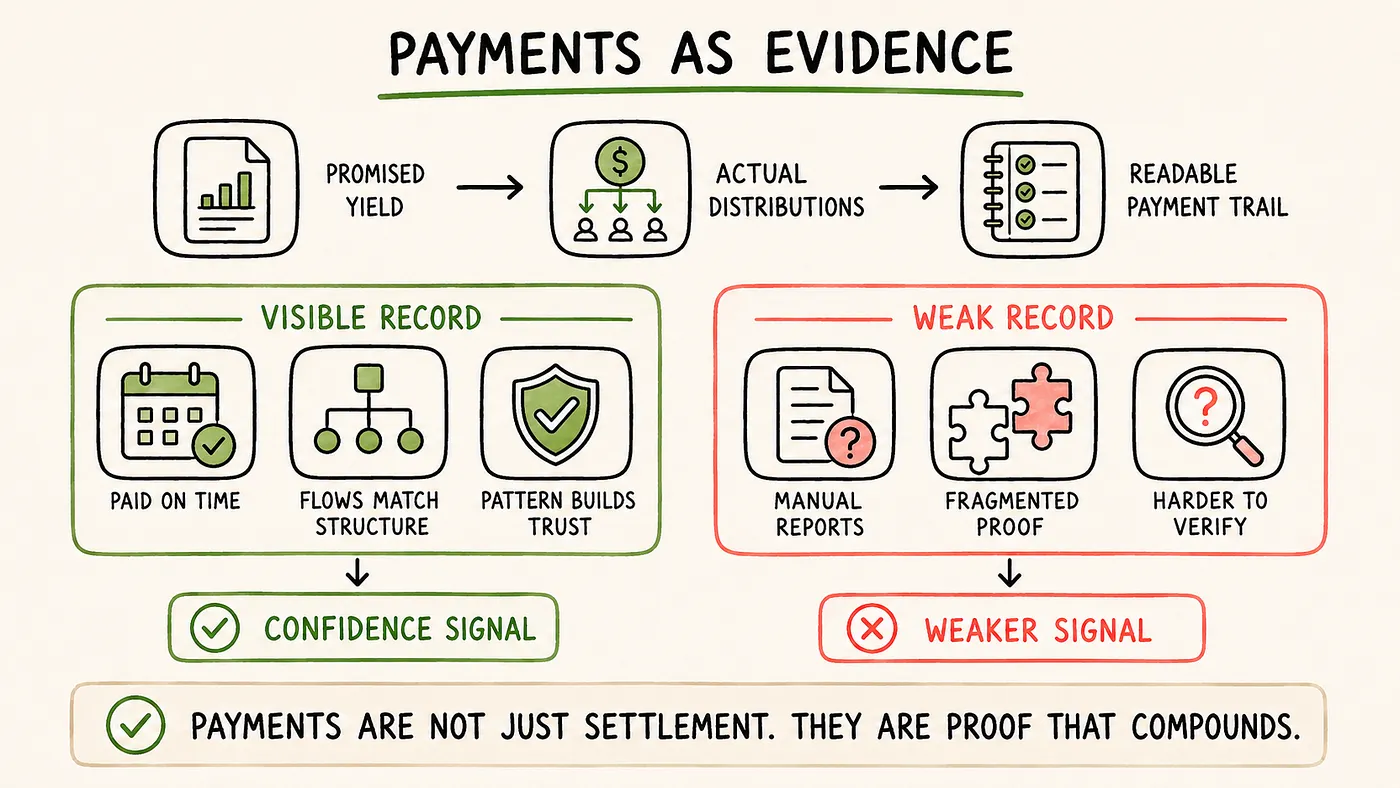

A promised yield is one thing and a visible distribution record is

something else, because the latter does much more work in a secondary

market by turning a claim into a pattern. A projected return is easy

to present, a readable payment trail is harder to fake, and that

asymmetry is exactly why it matters more to a buyer who wasn't there

at the start.

Tokenized assets still struggle for exactly this reason when payment

logic isn't tightly tied into the asset's readable history. If

payments happen but the record stays fragmented, delayed, or dependent

on separate manual reporting, the market can't use them properly as

trust signals. The value is there but the evidence remains weaker than

it should be.

Payments are not simply operational outputs, they're part of the

asset's record, and once that record becomes more visible and more

durable the market has something stronger to work with. That is really

important for later financing, later buyers, and later confidence.

It's not only about settlement, it's proof that compounds, and that's

considerably more valuable than the market currently treats it.

The market likes to talk about cross-chain access as if broader reach

automatically helps liquidity.

Sometimes it does, but often it only shifts the problem around. If an

asset can move into another ecosystem but the buyer on the other side

still has to rebuild confidence from scratch, the extra reach does

less than people hope. The token travelled, but the market confidence

didn't, and that's a distinction the market consistently underweights.

A business owner sees broader distribution, a buyer still sees an

asset that needs too much reconstruction, and the market becomes

technically wider without becoming materially deeper.

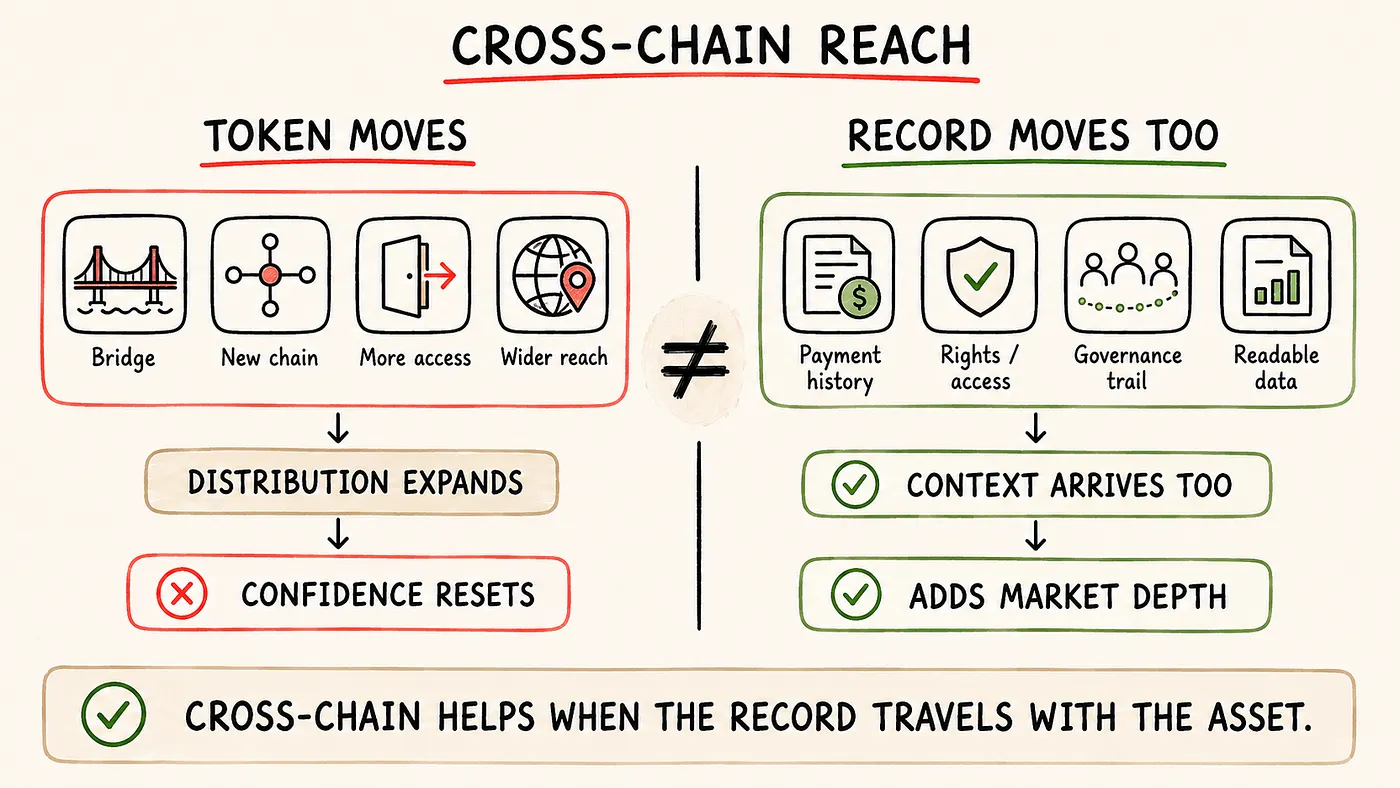

A stronger model is one where the record travels with the asset.

Later buyers, even in new markets or new environments, should be able

to understand what they are buying, as opposed to just seeing a

transferable ownership marker. That means carrying the relevant

payment history, entitlement logic, governance trail, and

identity-linked eligibility where it is most important, and these are

the details that make an asset easier to evaluate, rather than just

easier to list somewhere else.

Uptick's cross-chain architecture makes a more specific argument than

standard multi-chain positioning. UCB and IBC handle the movement, but

the commercially meaningful part is whether decentralized data

services, DID-linked access logic, and payment records move with the

asset in a form that still makes sense on the other side.

These are the pieces that make Uptick's roadmap more interesting than

standard cross-chain positioning, because the real question is whether

an asset that originated in one environment can arrive somewhere new

without destroying the operating history that makes it readable.

If it can, every new environment the asset reaches becomes additive to

market depth rather than another place where confidence has to be

rebuilt from nothing, and that's where cross-chain starts becoming a

market-strengthening layer rather than just a distribution play.

A market starts feeling liquid when later participants are no longer

forced into a weak informational position.

The logic from there is fairly straightforward, because the more

readable the asset becomes, the less expensive confidence becomes, and

the less expensive confidence becomes, the wider the buyer pool gets.

That's what deepens a market, not perfectly, not instantly, but

structurally.

This is why so many tokenized assets still don't feel liquid even

though the rails keep improving. The informational disadvantage for

later buyers is still too high, the market still asks for too much

blind trust, too much reconstruction, and too much dependence on

whoever already controls the context, and that problem doesn't get

solved by adding more transfer infrastructure on top of it.

The secondary market question matters because it forces the whole

category to stop admiring the wrapper and start judging the record,

and it forces the market to ask whether this asset has become easier

to understand over time or whether it still needs too much explanation

to sustain broader participation.

That's a better question than whether it's tradable, because real

liquidity is what happens when later buyers stop feeling like

outsiders to the truth of the asset.

Most tokenized assets still don't feel liquid for a simple reason, and

it isn't the transfer layer, which has improved considerably. The

problem is that confidence hasn't kept pace with transferability. An

asset can move, but if the history is fragmented, payments are hard to

read, governance is opaque, and the asset still depends on issuer

explanation more than market-readable evidence, later buyers can't

step in with real conviction, and the market stays thinner than people

expected.

Secondary markets aren't built on tradability alone. They're built on

readable history, visible operating behaviour, and a lower cost of

confidence for the buyer who comes later. That's a harder standard

than most of the category is currently meeting, and it's the one that

actually determines whether a market develops depth or just the

appearance of it.

Liquidity has always been an information problem rather than an

infrastructural one, and the category has spent most of its energy on

the wrong layer. Uptick's bet is that the assets which eventually

develop real secondary market depth will be the ones where the record

accumulated cleanly over time, where each cycle added to what the next

buyer could read rather than adding to what they had to reconstruct,

and where the infrastructure underneath made that possible without the

issuer having to manually hold it together.

That is a completely different kind of infrastructure goal than most

of the category has been chasing, but it's the right one.